There are many who take careful notice of the GlobalEurope Anticipation Bulletin (GEAB). I too, have often found it interesting, and insightful.

The latest GEAB is certainly worth reading, and heeding. But not for the obvious, headline reason.

It may be flagging in advance a “reform” agenda, to be triggered as a response to a new, bigger crisis. A reform that some, including myself, have long expected (excerpt-only below):

A situation which is now out of control

The illusions which have still blinded the last remaining optimists are in the process of dissipating. In previous GEAB issues we have already laid out the world economy’s grim picture. Since then the situation has got worse. The Chinese economy confirms its slowdown (1) as well as Australia (2), emerging countries’ currencies are disconnecting (3), bond interest rates are rising, UK salaries are continuing to fall (4), riots are affecting Turkey and even peaceful Sweden (5), the Eurozone is still in recession (6), the news filtering out of the United States is no longer cheerful (7)…

Nervousness is now clearly palpable on all financial markets where the question is no longer knowing when the next record will be but succeeding in getting out soon enough before the stampede. The Nikkei has fallen more than 20% in three weeks during which there have been three sessions with losses exceeding 5%. So, the contagion has now reached the “standard” indices such as the stock exchanges, interest rates, and currency exchange rates… the last bastions still controlled by the central banks and, therefore, totally distorted as our team has repeatedly explained.

In Japan this situation is the result of the over-the-top sized quantitative easing programme undertaken by the central bank. The Yen’s fall has brought about strong inflation in the price of imported goods (particularly oil). The huge swings in the Japanese stock exchange and currency is destabilising the whole of global finance. But the implementation of the Bank of Japan’s programme is so new that its effects are still much less pronounced than those of the Fed’s quantitative easing. It’s primarily the Fed which is responsible for all the current bubbles: real estate in the United States (8), stock exchange record highs, bubbles in and destabilisation of emerging countries (9), etc.

It’s also thanks to it, or rather because of it, that the virtual economy has got going again with even greater intensity and that the necessary balancing hasn’t taken place. The same methods are producing the same effects (10), an increased virtualisation of the economy is leading us to a second crisis in five years, for which the United States is once again responsible. The central banks can’t hold the global economy together indefinitely; at the moment they are losing control.

A second US crisis

If the months of April-May, with a great deal of media hype, seem to agree with the US-UK-Japanese method of monetary easing (to put it mildly) against the Euroland method of reasoned austerity, for several weeks now the champions of all-finance have had a little more difficulty in claiming victory. The IMF, terrified by the global impact of the economic slowdown in Europe, doesn’t know what else to come up with to force Europeans to continue spending and make deficits explode again: even empty boutique World must continue to give the impression that it’s still in business, and Europe isn’t playing the game.

But the toxic effects of central bank operations in Japan, the United States and the United Kingdom now demolish the argument (or rather propaganda) touting the success of the “other method”, supposed to allow recovery in Japan, the US and the United Kingdom (incidentally, the latter has never even been mentioned).

The currently developing second crisis could have been avoided if the world had taken note that the United States, structurally incapable of reforming itself, was unable to implement other methods than those which had led to the 2008 crisis. Like the irresponsible “too big to fail” banks, the “systemically” irresponsible countries should have been placed under supervision from 2009 as suggested from the GEAB n° 28 (October 2008). Unfortunately the institutions of global governance have proved to be completely ineffective and powerless in managing the crisis. Only regional good sense has been able to put it in place; the international arena producing nothing, everyone began to settle their problems in their part of the world.

The other crucial reform advocated (11) since 2009 by the LEAP/E2020 team focused on taking a completely new look at the international monetary system. In 40 years of US trade imbalances and the volatility of its currency, the dollar as the pillar of the international monetary system has been the carrier of all the United States’ colds to the rest of the world, and this destabilising pillar is now at the heart of the global problem because the United States is no longer suffering from a cold but bubonic plague.

Absent having reformed the international monetary system in 2009, a second crisis is coming. With it comes a new window of opportunity to reform the international monetary system at the G20 in September (12) and one almost hopes that the shock happens by then to force an agreement on this subject, otherwise the summit risks taking place too soon to gain everyone’s support.

——–

Notes:

(1) Source: The New York Times, 08/06/2013.

(2) Source: The Sydney Morning Herald, 05/06/2013. Read also Mish’s Global Economic, 10/06/2013.

(3) Source: CNBC, 12/06/2013.

(4) Source: The Guardian, 12/06/2013.

(5) Read Sweden’s riots, a blazing surprise, The Economist, 01/06/2013.

(6) Source: BBC News, 06/06/2013.

(7) Read Economic dominos falling one by one, MarketWatch, 12/06/2013.

(8) A bubble in current market conditions; normally this would be considered a thrill. Market Oracle, 10/06/2013.

(9) On the consequences of worldwide QE in India: Reuters, 13/06/2013.

(10) The return of financial products at the origin of the 2008 crisis is not insignificant. Source : Le Monde, 11/06/2013.

(11) Cf. GEAB n°29, November 2008.

(12) Source: Ria Novosti, 14/06/2013.

Hmmmmm.

September 2013.

That would be convenient timing.

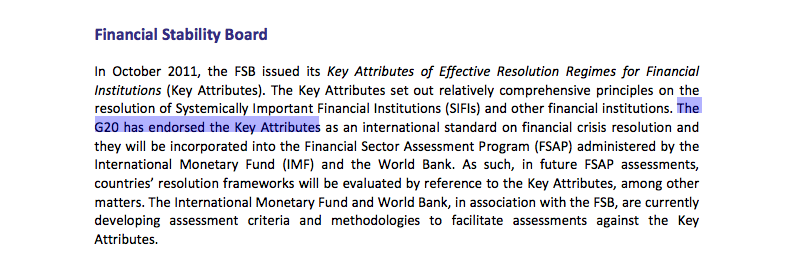

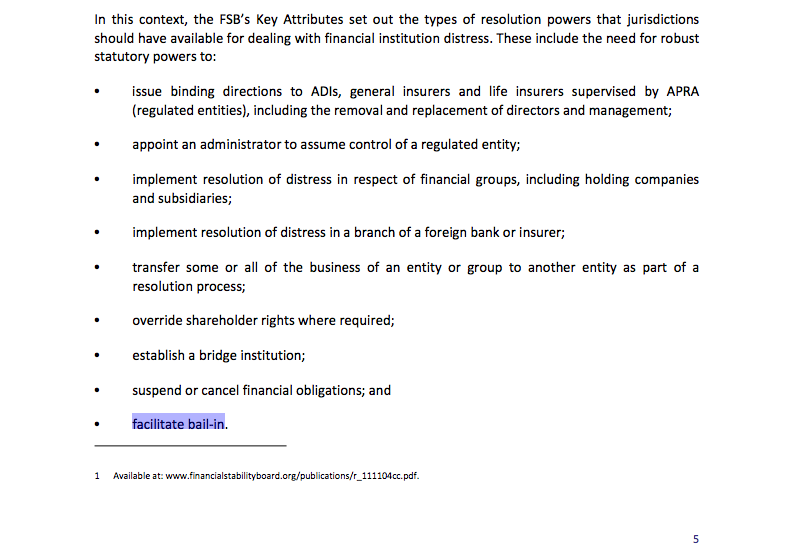

Since we have now seen the irrefutable evidence that, as agreed at Seoul in 2010, the G20 nations — in particular, the EU, UK, USA, Canada, Australia, and New Zealand — are all now well advanced in their preparations to implement a Cyprus-style “bail-in” of banks.

See Timeline For “Bail-In” Of G20 Banking System.

I’ve said it before, and will again.

Any “new” monetary system that is suggested by the usual suspects — the internationalist IMF, World Bank, FSB, etc, which are all little more than elitist bankster covens — is NOT the new monetary system we should want.

Because it would only ever be, as now, their system. Of their design. For their benefit.

What the world needs is something very different to anything that the bankers would ever promote –

Imagine A World With No Banks

“Money has no motherland; financiers are without patriotism and without decency; their sole object is gain.”

– Napoleon, 1815

Tags: GEAB, GFC, IMF, leap2020, monetary system, reserve currency

Comments