Tags: ALP, asylum seekers, election 2013, kevin rudd, Labor Party, pink batts

What. A. Total. Wanker.

7 Jul The Ego has landed:

The Ego has landed:

Mr Rudd said today he was happy to be returning to Indonesia, where he’d been on at least 10 previous occasions both as “a somebody” and “a nobody”.

“I’m back to being a somebody,” he said.

Oh, right.

I get it.

Unless you’re the PM, you’re “a nobody”.

Thanks for letting us all know, Kev.

*cough* WANKER! *cough*

I wonder why your PMO staff neglected to include that bit in the official transcript of your speech:

FRI 05 JULY 2013

Prime Minister

Jakarta, Indonesia

In 2007 – less than a month after I became Prime Minister – Indonesia was the destination of my first overseas visit.

Today, in 2013, I am pleased to return here once again in my capacity as Prime Minister and to meet again with my counterpart, and good friend, President Yudhoyono.

In these five-and-a-half years, I have been to Indonesia ten times.

This is a beautiful country.

Thérèse and I love this country and its people.

And it is good to be back again.

UPDATE:

Yes, he really did say it (ABC Lateline video here):

TRANSCRIPT

TOM IGGULDEN, REPORTER: There was a touch of triumphalism about Kevin Rudd’s trip to Indonesia.

KEVIN RUDD, PRIME MINISTER: I’ve been back here 10 or 11 times, in one capacity or another. As a somebody and as a nobody, and back to being a somebody.

Mortgage Insurance Through The Roof, And Other Nasty Signs

7 JulFrom the Sunday Telegraph:

PREMIUMS have gone through the roof for the supposed “insurance” that a quarter of all homebuyers have to pay when taking out a loan.

Lenders Mortgage Insurance for a borrower with a typical 10 per cent deposit on a $500,000 property has risen from less than $6000 last year to nearly $9000, a surge of close to 50 per cent according to brokers Home Loan Experts.

… LMI has been used in more than two million loans but is poorly understood and is rarely discussed in detail. It is charged whenever a borrower has a deposit of less than 20 per cent. Many of those who pay it don’t even realise it protects the bank, not them.

In August 2011, then Treasurer Wayne Swan announced the introduction of a one-page fact sheet on LMI. Nearly two years on it still isn’t in place. It is “close” to being in place, according to the office of Assistant Treasurer David Bradbury.

Incredibly, when it is, it won’t even nominate the cost. And it is unlikely to point out that LMI is neither portable nor refundable.

That means any household looking to refinance with another lender faces paying thousands of dollars in LMI for a second time, unless they have at least 20 per cent equity in their home.

Mortgage brokers and consumer groups say this is undermining the Government’s efforts to increase competition in the home-loan market because having to pay LMI again makes switching lenders financially unviable.

… Home Loan Experts’ LMI premium increase calculations were based on comparing 2012 and 2013 rates for Genworth, one of the two major providers of lenders mortgage insurance in Australia.

When contacted for comment, Genworth said all executives authorised to speak to the media were on holidays.

Premiums levied by the other big provider, QBE, have also increased considerably. A mortgage broker who asked not to be named for fear of retribution said there had been a 17 per cent increase since 2010…

QBE would not provide any information on its premium rates. However, a spokeswoman did say premium increases were due to elevated claim levels and higher reinsurance costs, as well as lower investment income.

Lenders Mortgage Insurance is a perfect example of how our society is totally ruled by bankers.

Consider for a moment just how completely unjust … how utterly f***ed up … “our” financial system is:

- Banks are (exclusively) allowed to create new “credit” — backed by nothing — simply by typing new numbers into their computer.

- Banks are allowed to make profits by charging usury (interest) on that new “credit”, when they sign you up to a loan contract — which you must repay, or risk losing everything you own (bank-rupt).

- You have to pay for insurance to protect the bank in the event that you can not continue repayments of their “credit” + usury.

- You have to pay for that insurance again, if you want to transfer your 30-year debt+usury repayment obligations to a different bank.

The “finance” game is completely rigged.

They can’t lose.

In related news, the real estate industry lobby parasites are now calling on the government to let first home buyers tap into their superannuation savings, in order to come up with enough money for a deposit:

Call to supersize home deposits

Concerned about declining home ownership levels and a sharp fall in the proportion of buyers purchasing their first property, the Real Estate Institute of Australia (REIA) wants first homebuyers to be able to tap into their superannuation savings to help them scrape together a deposit.

… The institute says recent interest rate cuts have had little impact on the desire of potential first homebuyers to enter the market.

Er … hello?! Maybe that’s because Australian house prices — the highest on the planet — are simply too expensive?

Maybe it’s because the younger, internet-savvy generations are discovering the truth about our world-leading housing Ponzi?

Or maybe it’s because they do not want to be in debt to the bankers usurers for the rest of their working lives?

The institute cites two schemes operating overseas – in Singapore and Canada – that allow first homebuyers to use their superannuation savings when they buy a property.

… The REIA has also called on state and territory government to reverse the trend to only offer first homebuyers grants for new dwellings. “It’s excluding 80-odd per cent of people who have historically bought established homes,” [REIA President Peter] Bushby says.

When it comes to keeping the flow of property buyers coming in at the bottom of the Great Australian Housing Ponzi scheme, supporting and driving up prices (and thus, their commissions from property sales), there really is nothing — no bald-faced lie, no cunning deceit, no twisting of the truth — that these filthy rotten morally vacuous scumbags won’t say.

Perhaps it would be best for the common good if these people — along with the bankers, whose scraps they feed off — were all rounded up, taken down the back paddock, and their 100% self-serving thought processes “rebalanced” the good old-fashioned way.

With a small high velocity lead weight implanted in the side of their heads.

If you are not keenly interested in understanding and sharing the truth about the evil, deceitful, parasitic way in which the bankers’ debt-at-usury “money” system works, then you — your apathy, your ignorance, your disinterest — are a vital part of the reason why this predatory, cancerous system continues.

Electro-Physics: The Theory Of Economic Warfare

6 Jul

Click to enlarge

We all know that mainstream economists are usually wrong.

But did you ever get the feeling that perhaps all the gobbledygook spouted by economists in support of their latest “analysis” and predictions, was — possibly unbeknown even to those economists — little more than an intellectual distraction? An obsession with trees, by those who are, despite sitting in ivory towers, unable to see the forest? A mass of abstractions, assumptions, and guesstimations, serving only to obscure the truth about economic reality?

If so, then the following excerpts will not only confirm your intuition. They will shine a blazing spotlight on the reality of mainstream economics theory — and practice — post-WW2.

And much more besides.

These excerpts are only a small portion of what is a lengthy, and far more technical document. One purportedly discovered on July 7, 1986 in an IBM photocopier purchased at a surplus sale.

I have chosen to quote only some of those few sections that might be more approachable to the typical reader of this blog. Those interested in far more detailed theoretical, mathematical, and technical information will find much food for thought and analysis in the full document (linked at the conclusion).

My bold emphasis is added:

Energy

Energy is recognized as the key to all activity on earth. Natural science is the study of the sources and control of natural energy, and social science, theoretically expressed as economics, is the study of the sources and control of social energy. Both are bookkeeping systems: mathematics. Therefore, mathematics is the primary energy science. And the bookkeeper can be king if the public can be kept ignorant of the methodology of the bookkeeping.

… the objective of economic research, as conducted by the magnates of capital (banking) and the industries of commodities (goods) and services, is the establishment of an economy which is totally predictable and manipulatable.

General Energy Concepts

In the study of energy systems, there always appears three elementary concepts. These are potential energy, kinetic energy, and energy dissipation. And corresponding to these concepts, there are three idealized, essentially pure physical counterparts called passive components.

- In the science of physical mechanics, the phenomenon of potential energy is associated with a physical property called elasticity or stiffness, and can be represented by a stretched spring.In electronic science, potential energy is stored in a capacitor instead of a spring. This property is called capacitance instead of elasticity or stiffness.

- In the science of physical mechanics, the phenomenon of kinetic energy is associated with a physical property called inertia or mass, and can be represented by a mass or a flywheel in motion.In electronic science, kinetic energy is stored in an inductor (in a magnetic field) instead of a mass. This property is called inductance instead of inertia.

- In the science of physical mechanics, the phenomenon of energy dissipation is associated with a physical property called friction or resistance, and can be represented by a dashpot or other device which converts energy into heat.In electronic science, dissipation of energy is performed by an element called either a resistor or a conductor, the term “resistor” being the one generally used to describe a more ideal device (e.g., wire) employed to convey electronic energy efficiently from one location to another. The property of a resistance or conductor is measured as either resistance or conductance reciprocals.

In economics these three energy concepts are associated with:

- Economic Capacitance – Capital (money, stock/inventory, investments in buildings and durables, etc.)

- Economic Conductance – Goods (production flow coefficients)

- Economic Inductance – Services (the influence of the population of industry on output)

All of the mathematical theory developed in the study of one energy system (e.g., mechanics, electronics, etc.) can be immediately applied in the study of any other energy system (e.g., economics).

Mr. _________’s Energy Discovery

What Mr. _________ had discovered was the basic principle of power, influence, and control over people as applied to economics. That principle is “when you assume the appearance of power, people soon give it to you.”

Mr. _________ had discovered that currency or deposit loan accounts had the required appearance of power that could be used to induce people (inductance, with people corresponding to a magnetic field) into surrendering their real wealth in exchange for a promise of greater wealth (instead of real compensation). They would put up real collateral in exchange for a loan of promissory notes. Mr. _________ found that he could issue more notes than he had backing for, so long as he had someone’s stock of gold as a persuader to show his customers.

[Readers of my essay, The People’s NWO: Every Man His Own Central Banker will recognise here the reason why I — and many others — have argued that Usury is The Key to the whole economic system here described. In past times, it was primarily the offering of security for one’s money (gold/silver) that induced people to deposit their stored wealth in the vaults of the goldsmiths / money-lenders (bankers). In modern times, it is the offering of usury (interest) on bank deposits that “induce(s) people into surrendering their real wealth in exchange for a promise of greater wealth”. More importantly, it is the offering of usury on bank deposits that distorts and confuses our ability to understand the fundamental difference between, and critical need to separate the functions of, those conceptual elements labelled “currency” (medium of exchange), and “money” (store of value).]

Mr. _________ loaned his promissory notes to individuals and to governments. These would create overconfidence. Then he would make money scarce, tighten control of the system, and collect the collateral through the obligation of contracts. The cycle was then repeated. These pressures could be used to ignite a war. Then he would control the availability of currency to determine who would win the war. That government which agreed to give him control of its economic system got his support.

Collection of debts was guaranteed by economic aid to the enemy of the debtor. The profit derived from this economic methodology made Mr. _________ all the more able to expand his wealth. He found that the public greed would allow currency to be printed by government order beyond the limits (inflation) of backing in precious metal or the production of goods and services.

Apparent Capital as “Paper” Inductor

In this structure, credit, presented as a pure element called “currency,” has the appearance of capital, but is in effect negative capital. Hence, it has the appearance of service, but is in fact, indebtedness or debt. It is therefore an economic inductance instead of an economic capacitance, and if balanced in no other way, will be balanced by the negation of population (war, genocide). The total goods and services represent real capital called the gross national product, and currency may be printed up to this level and still represent economic capacitance; but currency printed beyond this level is subtractive, represents the introduction of economic inductance, and constitutes notes of indebtedness.

War is therefore the balancing of the system by killing the true creditors (the public which we have taught to exchange true value for inflated currency) and falling back on whatever is left of the resources of nature and regeneration of those resources.

Mr. _________ had discovered that currency gave him the power to rearrange the economic structure to his own advantage, to shift economic inductance to those economic positions which would encourage the greatest economic instability and oscillation.

[Regular readers will here find a powerful affirmation of the reason why your humble blogger has long advocated that only a correct understanding of the difference between “money” as store-of-value, and “currency” as medium-of-exchange, with resultant currency reform, can save the world from the predations of the usurers — that is, the money/currency/”credit” issuers. See Imagine A World With No Banks]

The final key to economic control had to wait until there was sufficient data and high-speed computing equipment to keep close watch on the economic oscillations created by price shocking and excess paper energy credits – paper inductance/inflation.

Breakthrough

The aviation field provided the greatest evolution in economic engineering by way of the mathematical theory of shock testing. In this process, a projectile is fired from an airframe on the ground and the impulse of the recoil is monitored by vibration transducers connected to the airframe and wired to chart recorders.

By studying the echoes or reflections of the recoil impulse in the airframe, it is possible to discover critical vibrations in the structure of the airframe which either vibrations of the engine or aeolian vibrations of the wings, or a combination of the two, might reinforce resulting in a resonant self-destruction of the airframe in flight as an aircraft. From the standpoint of engineering, this means that the strengths and weaknesses of the structure of the airframe in terms of vibrational energy can be discovered and manipulated.

Application in Economics

To use this method of airframe shock testing in economic engineering, the prices of commodities are shocked, and the public consumer reaction is monitored. The resulting echoes of the economic shock are interpreted theoretically by computers and the psycho-economic structure of the economy is thus discovered. It is by this process that partial differential and difference matrices are discovered that define the family household and make possible its evaluation as an economic industry (dissipative consumer structure).

Then the response of the household to future shocks can be predicted and manipulated, and society becomes a well-regulated animal with its reins under the control of a sophisticated computer-regulated social energy bookkeeping system.

Eventually every individual element of the structure comes under computer control through a knowledge of personal preferences, such knowledge guaranteed by computer association of consumer preferences (universal product code, UPC; zebra-striped pricing codes on packages) with identified consumers (identified via association with the use of a credit card and later a permanent “tattooed” body number invisible under normal ambient illumination).

[Who can dispute the evidence of the rise and rise of exactly this phenomenon today — Facebook, Amazon, YouTube, Google, indeed all the dominant players in the Internet Age use ever more sophisticated computer systems to monitor user behaviour, and gather information on users’ personal consumer preferences, in order to sell more products, or advertising space, or user data to governments and commercial entities.]

Summary

Economics is only a social extension of a natural energy system. It, also, has its three passive components. Because of the distribution of wealth and the lack of communication and lack of data, this field has been the last energy field for which a knowledge of these three passive components has been developed.

Since energy is the key to all activity on the face of the earth, it follows that in order to attain a monopoly of energy, raw materials, goods, and services and to establish a world system of slave labor, it is necessary to have a first strike capability in the field of economics. In order to maintain our position, it is necessary that we have absolute first knowledge of the science of control over all economic factors and the first experience at engineering the world economy.

In order to achieve such sovereignty, we must at least achieve this one end: that the public will not make either the logical or mathematical connection between economics and the other energy sciences or learn to apply such knowledge.

This is becoming increasingly difficult to control because more and more businesses are making demands upon their computer programmers to create and apply mathematical models for the management of those businesses.

It is only a matter of time before the new breed of private programmer/economists will catch on to the far reaching implications of the work begun at Harvard in 1948. The speed with which they can communicate their warning to the public will largely depend upon how effective we have been at controlling the media, subverting education, and keeping the public distracted with matters of no real importance.

***************************

This should be sufficient for the typical reader — and the serious economics enthusiast — to see a blazing ray of light.

For those interested in the theoretical/technical and mathematical foundations, subsequent topic areas include:

- The Economic Model

- Industrial Diagrams

- Three Industrial Classes

- Aggregation

- The E-model

- Economic Inductance

- Inductive Factors to Consider

- Translation

- Time Flow Relationships and Self-destructive Oscillations

- Industry Equivalent Circuits

- Stages of Schematic Simplification

- Generalization

- Final Bill of Goods

- The Technical Coefficients

- The Household Industry

- Household Models

- Economic Shock Testing

- Introduction to the Theory of Shock Testing

- Example of Shock Testing

- Introduction to Economic Amplifiers

- Short List of Inputs

- Short List of Outputs

- Table of Strategies

- Diversion, the Primary Strategy

- Diversion Summary

- Consent, the Primary Victory

- Amplification Energy Sources

- Logistics

- The Artificial Womb

- The Political Structure of a Nation – Dependency

- Action/Offense

- Responsibility

- Summary

- System Analysis

- The Draft

- Enforcement

Click here for the entire document.

h/t and thanks to reader Kevin Moore for bringing this to our attention.

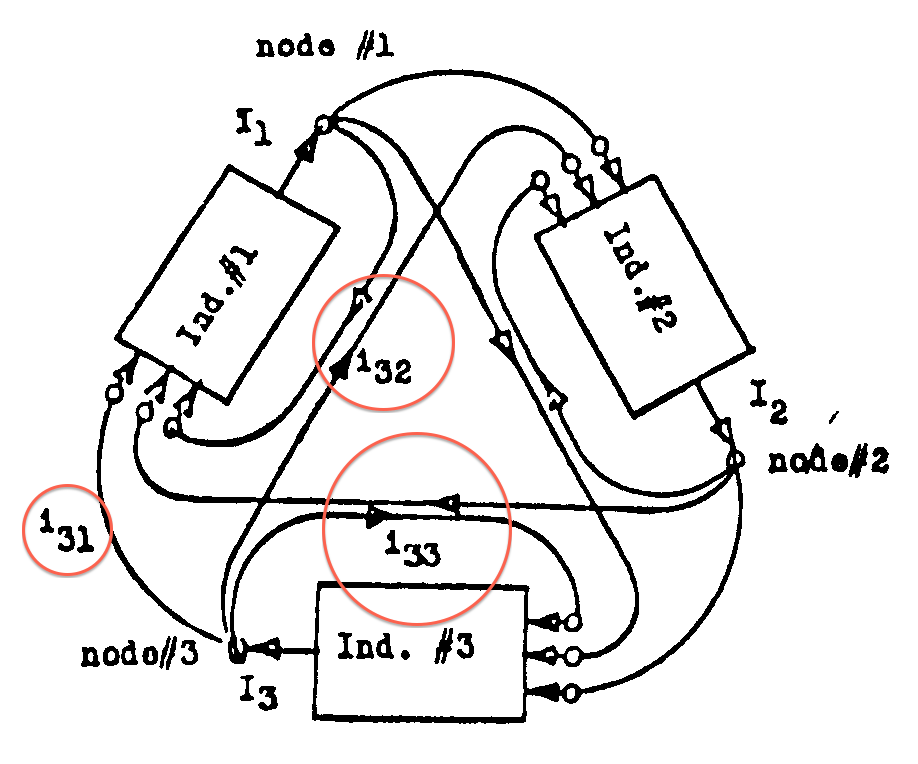

Finally, for conspiracy buffs with a keen eye, the following network diagram of the “three industrial classes” taken from the document may be of interest. Particularly the form (ie, shape), and, the numbers (circled in red):

Click to enlarge

Compare:

EU Confirms Plan For Cyprus-Style Theft of Bank Deposits

6 JulAs warned here repeatedly…

G20 Governments All Agreed To Cyprus-Style Theft Of Bank Deposits… In 2010

Federal Reserve Governor Confirms – Bank Depositors Will Be Cyprused

Growing Political Deception On Bank Deposits Theft

Federal Reserve Says Bank Bail-Ins Coming To The USA

… the internationalist banksters’ plan to set up a global regime for “resolution” of failing banks, wherein governments will give themselves free reign to “bail-in” the banks using depositors’ savings, is now slowly but surely being enacted by governments worldwide.

From The Telegraph (UK):

EU makes bank creditors bear losses as Cyprus bail-in becomes blue-print for rescues

New European Union “bail-in” rules to impose the losses of failed banks on shareholders, bondholders and some large depositors were agreed early this morning by Europe’s finance ministers.

…Jeroen Dijsselbloem, the chairman of the Eurogroup of finance ministers, hailed the agreement as a major step towards a “banking union” and away from state funded aid to recapitalise or bailout troubled banks across Europe.

…Greg Clark, the financial secretary to the Treasury, declared that Britain was happy with the new rules after securing concessions allowing governments flexibility on how to tailor bank “resolution” to national circumstances and existing British arrangements on banking levies.

…Under the deal, after 2018 bank shareholders will be first in line for assuming the losses of a failed bank before bondholders and certain large depositors. Insured deposits under £85,000 (€100,000) are exempt and, with specific exemptions, uninsured deposits of individuals and small companies are given preferred status in the bail-in pecking order for taking losses.

It is most important to recall what we have shown previously.

Do not be fooled into believing that, because Australia’s government has “guaranteed” (ie, insured) bank deposits up to $250,000, that this means your savings are safe, and that a failing Aussie bank will not be “bailed-in” using your money.

The government’s “guarantee” is limited, to just $20 billion per failed bank.

That’s less than one-tenth of the total amount of customer deposits — digital bookkeeping entries — actually “held” by Australian banks.

(see The Bank Deposits Guarantee Is No Guarantee At All )

To the best of my knowledge, Australia’s politicians have not yet begun to legislate the new, FSB-mandated and G20-agreed bank “bail-in” regime here.

But when they do, your savings will be exposed to confiscation.

Just as intended:

Earlier on Monday, Bank of England Deputy Governor Paul Tucker said the EU law on bank recovery and resolution would be a milestone towards a global system.

The Clinching Argument In The “Private vs Public Debt” Debate

5 Jul“He’s pretending that he’s elected by the people, and he’s actually elected by the banks”

In the following interview, Professor Steve Keen discusses how government “stimulus” or “help” programs that hand out borrowed (by the government) money to entice prospective house buyers, are actually Ponzi schemes.

But the most important truth of all is revealed from 10:14sec onwards:

INTERVIEWER: The Chancellor of the Exchequer, George Osborne, says he wants to reduce debt in Britain, while simultaneously launching the “Help To Buy” scheme which is an increase in debt. So my simple question is, Is the Chancellor lying?

KEEN: I think the Chancellor, like most politicians, is focussing on the level of government debt, not on the level of household and private debt, and they think that’s the real problem. The cause of this crisis was an out of control private banking sector lending to the private sector to encourage it to speculate on assets….

INTERVIEWER: (interrupts) Let me, let me, let me jump in for a second, because what we have found out in 2008 and going forward is that there really is no such thing as private debt, because when these private debts become unsustainable the private sector simply gives them to the government. So ultimately taxpayers always end up footing the bill for this debt, all the combined debt of household debt, bank debt, government debt, it’s all the same debt, that’s all underwritten by the same abused taxpayers, and the Chancellor — by ignoring this — is pretending that the UK people are brain dead!

KEEN: Well, what he’s pretending is that he is elected by the English people and he’s actually elected by the English banks. All this happens because the banks have got the politicians by the intellectual balls. They believe that the economy has to have a growing banking sector to be healthy, and that’s just like believing that you have to have a growing cancer to be a healthy human being. Past a certain stage the financial sector becomes a parasite. But it becomes such a strong and powerful parasite that the politicians think that if they let it die the economy will die. That’s precisely the opposite of the case — you’ve got to get the financial sector to shrink, you’ve got to cut it down, say in England, by a factor of at least 2 — and then in terms of abolishing debt, writing it off, not honouring the stuff, and standing up for the debtors, rather than standing up and voting for the creditors which, unfortunately, is what the politicians around the world have been doing this time around…

Unfortunately, Steve sidestepped the critical observation made by the interviewer — that because banksters simply palm off their out-of-control debt problems to the government, aided and abetted by compliant politicians, what this means is that, in the end, private debt and public debt must be considered in sum, not separately.

This is why Barnaby is right.

Although relatively “low” compared to that of “other advanced economies”, nevertheless Australia’s ever-rising public debt trajectory does matter a helluva lot.

Why?

Because — even though (sadly) Barnaby never points this out — Australia’s private debt levels are the highest in the world.

Our Household Debt sits around 150% of household disposable income.

Our government-guaranteed banking sector is massively leveraged to Australia’s world-leading house price Ponzi.

So, simply stated, because of our massive private debt problem, our nation absolutely cannot afford the added risk of an ever-rising public debt level too.

Usury And The Irrelevant Complicit Church

4

Jul

With thanks and h/t to reader Phil, the following article dated May 2010 is cross-posted from the Economic Edge:

Damon thinks this is one of the most important articles he’s written. I think it’s powerful and should get you thinking regardless of your personal views. I also think it’s important to note that he is addressing religion from this perspective, “We need to avoid dialectical conflict… left vs. right, religion vs. non-religion, black vs. white, immigrant vs. citizen, etc. We need to come together to fight the monetary powers that are bringing us all down together.”

Amen to that.

The Coming Crash: Usury and the Irrelevant Church

By Damon Vrabel

Please, let us stop this usury! – Nehemiah 5:10

It’s been a wild couple of weeks—increasing unemployment, Greek debt crisis, yet another ridiculous bailout, pressure on Goldman Sachs, accusations of commodities manipulation by JP Morgan Chase, and new freakish levels of market volatility that might be signaling the next phase of market collapse. The many day-to-day issues can leave us dazed and confused, so most people ignore them. Huge mistake.They are all related to the most powerful force on earth that controls our lives because it is the very foundation of our society—usury. We are ruled not by governments anymore but by financial powers that use interest-bearing debt to exert control over governments, corporations, and people. Almost all other political issues with which we concern ourselves are secondary symptoms of or purposeful distractions from this larger narrative that is never reported by the Wall-Street-funded media. Sadly the church has remained silent as well.Explaining the details can be extremely complicated, but the basic core to understand is that the US government issues no money. Instead all money comes from private banking institutions with interest attached. At times in the past the US government issued real money for people to use—US notes and coins. But today all money comes from the Federal Reserve’s private banking system by putting the US government, i.e. 308,000,000 Americans, in debt. If the US government were not in debt to the banking system, the American people would have no money.More technically, the Fed and its Wall Street cartel banks like JP Morgan Chase and Goldman Sachs make billions by doing nothing but controlling our money. They have the monopoly license to create the core money in our system from holding US Treasury bonds on their balance sheets. These bonds represent the debt of the United States. Thanks to interest, the bonds pull a large portion of our wages to the banks. The primary purpose of the IRS is to take your wages to pay the interest back to the banks. In effect, Wall Street owns a good bit of your labor. And the more bonds they hold, i.e. the more debt the population is in, the more money they make thanks to the interest flows and the profits from gambling on your debt. The system is very much one of “us vs. them.” Such is the nature of monopoly power and usury.

Economics and Morality

Controlling others and living off their backs by forcing them to borrow with interest in order to have any money is called usury (this does not include standard, self-liquidating bank loans to businesses to fund production). It is a system that ensures everything we do, whether in the public or private sector, feeds Wall Street and the controllers above it. It creates a two-tiered societal pyramid of money pushers on top vs. money users on bottom. The power differential is huge. Everyone is hostage. In doing something as simple as buying food to survive, we contribute to usury because we only have usury-based money, not real money. Like the slaves who built the Egyptian pyramids, today we are stuck building an invisible pyramid of monetary power.In such a system there is never enough money to pay back all the interest to the money pushers. The only solution is for the money users—government, corporations, individuals—to borrow more. This is the reason our debt continues skyrocketing to increasingly insane levels. It isn’t about politics, but the fundamental exponential math underlying the system—the users must borrow more and more to pay back interest and keep the system afloat. Such math is guaranteed to fail. Iceland and Greece have reached the point of failure. The rest of the Europe and the US will experience failure as well. Then we will see money and assets vacuumed up the pyramid by the money pushers—the banking establishment that owns the collateral and can take your property.The exponential math not only creates exponential debt growth, but also exponentially increasing:

- Scale – government and businesses keep getting bigger; we get smaller and local communities lose their meaning

- Velocity – the hamster wheel keeps spinning faster; human life suffers

- Consumption – we buy more and more things that break more quickly

- Production – we make more and more things that break more quickly

- Inflation – the dollar buys less and less; we can’t seem to make progress

None of these things have to happen in an economic system. They only happen in ours because of debt-based money, usury, that greatly benefits the top of the pyramid while everyone else suffers to a certain degree depending on their level in the pyramid.

So this system is guaranteed to fail due to not only the impossible math, but also the fundamental immorality. Taken together those five issues paint a horrible picture. Republicans blame Democrats and vice-versa. Nope. It’s all a very simple result of a system based on usury, which used to be considered profoundly immoral. It was a fundamental violation of every major religion. It still is for Islam, but Christianity succumbed long ago. They thought a free market economic system would be beneficial, but got snookered into thinking that usury had to be part of that system. On the contrary, monolithic usury kills the free market.

Our monetary system is a top-down controlling machine, not a free market. It is run not by government, but by the most powerful financial interests in the world. Some people feel in their guts that someone must be stealing from them because they just can’t get ahead no matter how hard they work. Well that’s because it’s true—someone is legally stealing from them. The simple math of usury pulls money from people on the bottom of the pyramid who create real value toward those at the top who create no value. MBAs and others serving the system must reckon with this truth rather than remaining blind. Farmers understand it well, having lost their property over the years to the bankers. Families feel it in the fact that it’s difficult to get enough money to feed the kids compared to 50 years ago when one parent could work a standard week and feed a family of five. Everyone in the system will feel it once the debt system collapses as it is doing in Greece.

Living off the backs of others was called feudalism 300 years ago. It was slavery 100 years ago. Today it’s called the “free market” thanks to the propaganda and fraud of neoclassical economics. It completely ignores the truth of our monetary system, the math behind it, and the eventual collapse that will result from it. Greece is giving us a glimpse, but it is only a mild pre-game warmup compared to what’s coming. The world will rue the day it was ever seduced into accepting usury and the illusion of prosperity driven by nothing but debt.

The Irrelevant Church

On this issue of monolithic usury, the issue from which many of our other problems spawn, the church seems to have no voice. Recently, an older church leader told me, “Keep it up, this needs to be addressed, but you have more guts than me, I don’t want to be killed.” Sobering comment, to be sure, but in the shadow of Gandhi, Dietrich Bonhoeffer, Oscar Romero, and Martin Luther King, is the church now impotent? Are its leaders now too afraid to speak truth to power, to stand against darkness? Or is the problem that the church is, like most of us, fooled by the myth that we live in a free market so we don’t realize we are immersed in an immoral system of controlling usury?

Lower class Greek citizens are now learning the painful truth about the mythical free market. A few of them have died as the police brutally repress them to enforce the usury system for the rich bankers like Goldman Sachs. Where is the voice of Bishop Romero? “I order you, stop the repression!” Iceland learned the lesson a few months ago. Several other populations have learned the lesson in the past as the controlling debt peddlers punished, conquered, and restructured their countries (Indonesia, Malaysia, Thailand, India, Argentina, Chile, Mexico, England, etc.). The same lesson is coming to the rest of Europe and the United States. But again, the church seems to be oblivious. It failed to heed Martin Luther King’s warning, “One of the great liabilities of history is that all too many people fail to remain awake…today our very survival depends on our ability to stay awake.” The church has fallen asleep.

The Dialectic of Left vs. Right

A possible reason is that the church has been co-opted by the manipulative left vs. right civil war created by the corporate media. In fact, Protestant denominations have split into conservative vs. liberal camps so they war against each other—Wall Street is brilliant at divide and conquer. Some sermons in conservative denominations sound like speeches from conservative politicians. Liberal Christian magazines sometimes seem to be just liberal political magazines with an added dash of Jesus.

Postmodernism should inform us that the left vs. right narrative is contrived to keep people from noticing the real power structure behind Wall Street that controls our lives. As long as the church submits to the false framework, church leaders will be “safe.” But that means they will also be irrelevant because they are not speaking to the primary narrative in our world that has always caused problems and is getting ready to unleash far more pain and poverty in the near future—the issue of monolithic usury and debt servitude. By not speaking against usury, the church has become a pawn of it. So the church has largely been conquered by the same concocted civil war that has divided society.

Dollar Tyranny

Another reason the church may be silent is the simple fact that it depends on money just like everything else does. Since all money in our system comes from usury, it is difficult to even notice it. And what authority would the church have to speak against it since it is itself complicit in it? Anybody or any organization that uses a Federal Reserve Note or a credit/debit card, which everyone must do, is unknowingly participating in usury because, again, all of that money comes from the bonds held by Wall Street. But knowingly or not, how could the church or any organization speak against the very thing that fuels its own existence?

The church’s tax-exempt status may be another reason for the silence. Tax exemption is one of the powerful ways the financial empire system influences and controls other entities. If the wrong person says the wrong thing, the IRS has the ability to suddenly remove the exemption, which doubles the cost of running that organization. The church never should have submitted to such tyranny over what may or may not be said.

Comfort of the Middle Class Bubble

Finally, it seems the comfort provided by the monetary system for the great mass in the middle, which is a key part of the church, keeps us from wanting to really think about it. The illusion of peace and prosperity that has lasted for so long has been nice. Some of us even thought we had that comfort because we were better people, so God blessed us. Reckoning with the truth will be painful for those who believe this. The fact is that our perceived comfort today is a result of the darkness of usury. The middle can only exist because there is a bottom that keeps our system afloat. They are the only reason the middle class exists. Moreover, the comfort is currently an illusion because most in the middle class don’t realize how indebted they are. Total unfunded liabilities currently hidden on the government’s financials put each American in an extra $300,000+ in debt that they currently aren’t aware of. That debt comes from the fact that, again, our money comes from usury.

Since the bubble was built on usury, its very existence is immoral, and everyone who participates in it becomes infected. It is also flimsy because usury means the bubble is sustained by debt. Many are already aware of the hollowness of the bubble since it has destroyed the fabric of our communities and a sense of deeper meaning in life. But others are able to ignore that and focus on the material comfort. What will happen to them once the material comfort itself crashes? It will soon. Some market forecasters predict the final collapse of our debt system will be worse than the Great Depression. The math is clear—it will be worse. Just like Greece, we will then see Wall Street paying the government to crackdown on the people, cancel social programs, and take their assets from them to hand them over to the upper class behind the banks. That is the end result of usury—using debt to control others and take their assets so they have no equity. At that point it will be too late for the church to save the lower and middle classes from violent repression and the upper class from their narcissistic detachment from the horror.

“Silence is Betrayal”

So is there a wing of the church that has not yet sold its soul? Is there a remaining Christian voice against usury, or are Muslims the only people in the world who stand against it? The church must wake up to the truth of our system and become relevant again. This is the civil rights issue of the 21st century, only this time it is not black vs. white but a few money pushers vs. the great mass of users. The power of the bond market is getting ready to wreak havoc. We’re all in it together this time. As Martin Luther King said, “There comes a time when silence is betrayal….That time has come for us today.” Will the real church please speak up?

Damon added the following commentary, “We are heading toward a very dark future, unless we fix it, because our system is built on a fundamental evil–usury. This force has taken over not just our economic system, but our governments, our lives, and everything else from schools, to nonprofits, to families, and even the church. I hope the word gets out on this one. And if you attend a church, regardless of religion or denomination, I think the leadership needs to be informed about this.”

***************

For readers interested in further research on this topic area, your humble blogger recommends Michael Hoffman’s excellent book, Usury In Christendom: The Mortal Sin that Was, and Now Is Not.

See also:

- Usury Centralises Wealth

- Looking For A Root

- Turning A Human Being Into This…

- Abuses Stript And Whipt

- Usury In Christ’s Kingdom?

- Usury – The Golden Age Of Big Money Oligarchy

- A Tale Of Usury, Explosions, And A Used Car Salesman

- Babylon = Usury: We Want Interest-Free Money

There’s No Other Game In Town: Banking Fraud (But I Repeat Myself)

2 Julh/t reader Kevin Moore for the following story, from presstv.ir –

Top Vatican bank officials resign after arrest of senior Italian cleric

The director and deputy director of the Vatican Bank have resigned after a senior Italian priest with close ties to the bank was arrested on suspicion of fraud and corruption.

In a statement issued on Monday, the Vatican announced that the bank’s director, Paolo Cipriani, and his deputy, Massimo Tulli, had stepped down.

On Friday, Italian authorities arrested a senior cleric known as Nunzio Scarano after an investigation of the bank, also known as the Institute for Works of Religion (IOR), produced evidence showing it may have been involved in an international fraud scheme.

Scarano was arrested along with Giovanni Maria Zito, a former Italian intelligence agent, and Giovanni Carinzo, a financial broker.

Prosecutors say Scarano paid Zito 400,000 euros ($523,000) to transport 20 million euros in cash from Switzerland to Italy onboard Zito’s private jet…

The Italian daily La Repubblica reported that Scarano is also under investigation in the city of Salerno on suspicion of money laundering.

Only priests, religious, Catholic institutions, employees of the Vatican City State, and diplomats accredited to the Holy See are allowed to have accounts at the IOR, but Italian politicians and organized crime figures allegedly also have accounts at the bank.

Over the years, the Vatican Bank has been involved in a series of scandals.

The bank’s governor in the 1980s, Archbishop Paul Marcinkus, was indicted over his involvement with the collapse of Italy’s largest private bank, Banco Ambrosiano, which was owned in part by the Vatican Bank.

In the aftermath of the scandal, the chairman of the bank, Roberto Calvi, was found hanged under Blackfriars Bridge in London in 1982. Calvi was known as God’s Banker because of his close ties to the Vatican. The death was initially ruled a suicide but later prosecuted as a murder.

The activities of the infamous P2 Masonic lodge were brought out of the shadows by the collapse of Banco Ambrosiano. Some investigative journalists suspected that some of the plundered funds went to P2 or to its members.

Propaganda Due, or P2, was a Masonic lodge operating under the jurisdiction of the Grand Orient of Italy from 1945 to 1976. P2 was sometimes referred to as a “state within a state” or a “shadow government.”

And still the greatest banking fraud of all — usury — goes on.

Unchecked, and unchallenged.

With the heretical support of the Roman Catholic Church, and indeed, pretty much all of modern-day Churchianity.

Aussie Jobs For Aussie Workers? Not In Our Capitalist Corporatocracy

2 JulFrom Tim Colebatch at The Age:

Rudd’s efforts to reach out to business have got nowhere. Some groups made impractical demands for Labor to withdraw its legislation to stop rorting of section 457 visas – which, as I reported earlier, has meant that in two years Australian-born workers have gained just 34,000 new full-time jobs. Brendan O’Connor as minister deserves credit for trying to restore the integrity of the system so that it operates as intended.

See also Colebatch’s earlier article, The books are being cooked on 457 visas –

Last month Immigration Minister Brendan O’Connor announced new reforms to stop alleged rorting of section 457 visas. Prime Minister Julia Gillard then beefed up the issue by telling western Sydney the reforms would stop ”foreign workers being put at the front of the queue with Australian workers at the back”.

Since then Gillard’s opponents have claimed she is out to destroy the 457 visa program, which allows business to import temporary workers at will if they cannot find suitable workers in Australia. And at the other extreme, some tell us the whole 457 program is a rort allowing business to bring in foreign workers to undercut wages and save firms from the need to invest in training their own workers.

So far Gillard seems to be losing the debate; but then, she usually does. What do the figures show?

They show that while demand for section 457 visas had declined in most sectors with the slowing economy – visa applications from mining companies are down 15 per cent so far in 2012-13 – that is outweighed by surging demand in other industries that seems at odds with what we know about how they are faring.

For example:

Until mid-2011, few firms used 457 visas to import cooks; in 2010-11, just 45 visas a month were issued for skilled kitchen staff. Yet by January this year, 1690 cooks had been granted 457 visas, 240 a month. Cooks have suddenly become the biggest users of section 457 visas.

Why? It’s not because of any surge in demand. The Bureau of Statistics estimates that spending in hotels and restaurants fell 1.1 per cent last year, as Australians economised on discretionary spending to avoid more debt. Where is the labour shortage that requires us to suddenly import thousands of foreign cooks?

It’s not just cooks. This year alone, the number of chefs, their superiors, entering on 457 visas has shot up 150 per cent to almost 90 a month. Imports of cafe and restaurant managers have quintupled, from 27 a month to 134 a month. Does anyone smell a rat here?

Digging right down to the true root of the problem, I blame usury.

The central evil in our wonderful world of “capitalist” “competition”.

It means the “survival of the fittest”, you see — another pernicious doctrine.

The “fittest” are those most willing and able to borrow and then repay the banks their debt “money” … plus usury.

Comments